Preview: Due May 15 - U.S. April CPI - Core rate not quite as strong as the preceding three months

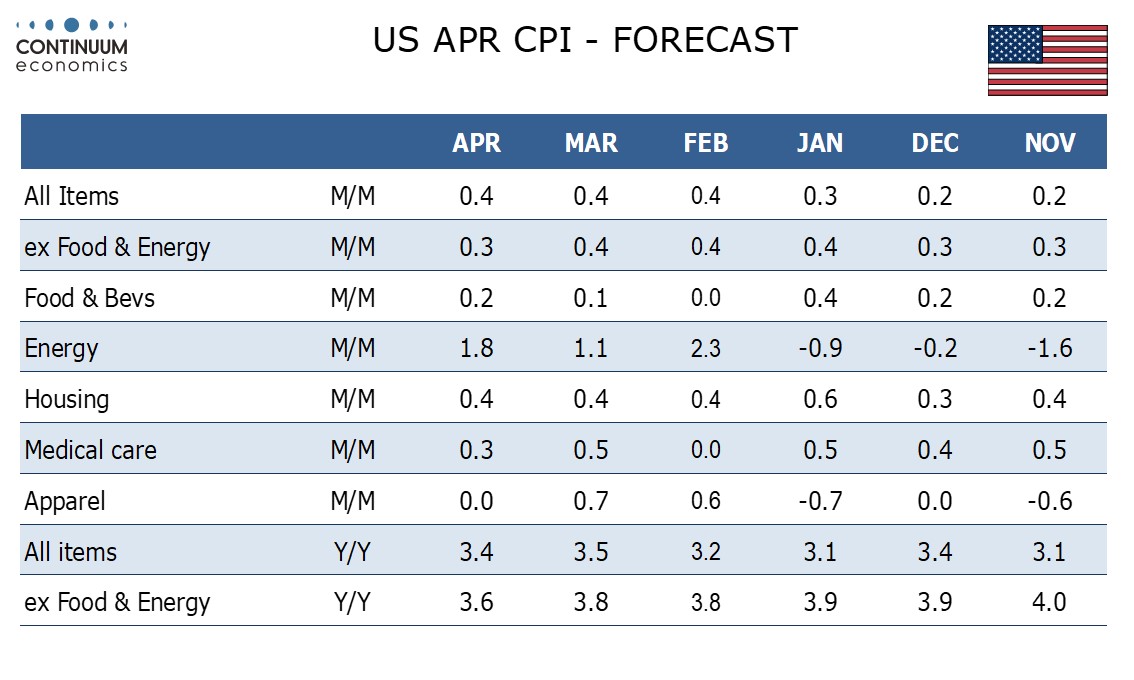

We expect April CPI to rise by 0.4% overall for a third straight month but with the ex food and energy pace slowing to 0.3% after three straight months at 0.4%. We expect the strong start to the year to fade as the year progresses, though inflationary pressures will still look quite significant in April.

January, when core CPI rose by 0.39% before rounding, is a particularly high risk month as New Year pricing decisions are made, but as activity picks up in the spring risks persist. February and March both rose by 0.36% before rounding meaning that not much slowing is needed to bring a 0.3% outcome before rounding, and we expect a 0.31% core CPI in April.

The main upside influence in April was a 2.6% surge in auto insurance, above even a strong trend and we expect April’s data to see some moderation, while two straight above trend gains in apparel are also unlikely to be repeated. Used auto prices look set to continue moving lower. One volatile component that could see upside risk is air fares if feed through from higher energy prices is seen. Air fares are likely to be stronger than March’s marginally negative outcome which corrected a very strong February. We expect fewer strong upside influences in April than in the first three months of the year.

Even with some restraint from seasonal adjustments, we expect a 1.8% rise in energy led by a 3.0% increase in gasoline to add almost 0.1% to the CPI. Food we expect to see a modest 0.2% increase. This will see yr/yr growth slowing to 3.4% from 3.5% overall and to 3.6% from 3.8% ex food and energy, the latter reaching its lowest since April 2021..